by Lauren T. Konagel | Feb 15, 2024 | Business and Personal, News

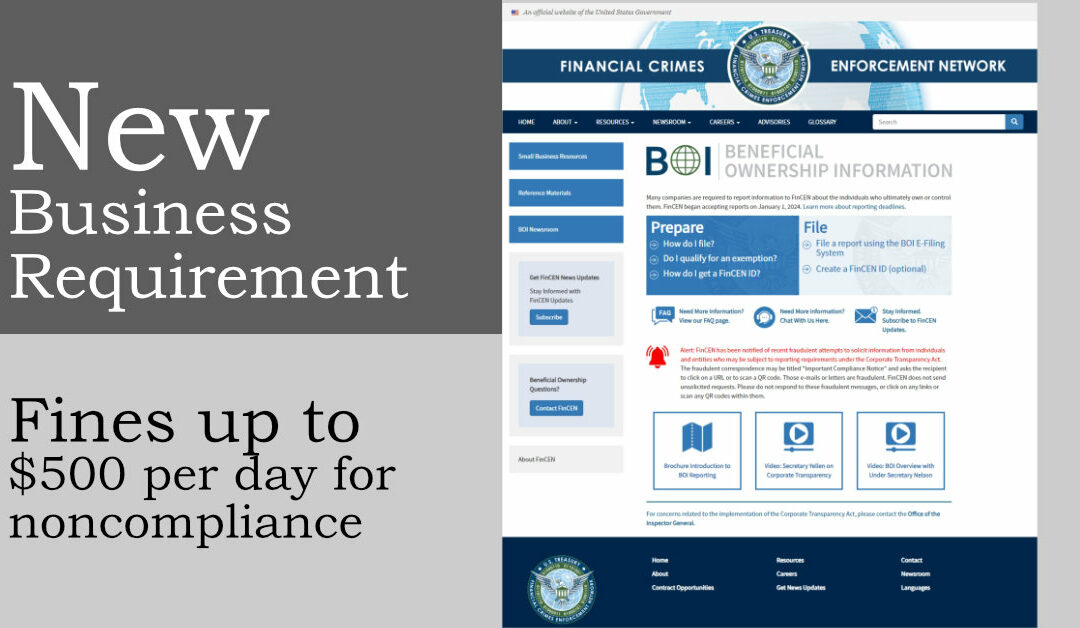

Beginning January 1, 2024, the Corporate Transparency Act (the “Act”) went into effect. Under the Act, all entities formed or registered to do business in the United States will either need to: Confirm they qualify for an exemption from the Act’s reporting... read more

by Lauren T. Konagel | Jul 25, 2023 | Business and Personal, Lauren T. Konagel

In today’s fast-paced and competitive business world, companies face numerous legal challenges on a daily basis, even when it may not seem obvious. From contract negotiations to intellectual property issues, regulatory compliance, and employment disputes, legal... read more

by Burke Costanza & Carberry LLP | Apr 5, 2023 | Business & Commercial Litigation, Business and Personal, Commercial Services, Litigation, News

Northwest Indiana Business Magazine Has Announced Best of Business Awards 2023. Each year, the magazine surveys their readers asking them to vote for the best businesses throughout Northwest Indiana and Greater South Bend / Mishawaka. The survey provides readers... read more

by Chad W. Nally | Feb 17, 2023 | Business and Personal, Commercial Services

Background Under the Bankruptcy Code, 11 § U.S.C. 547(b)(4)(A) provides that, with a few exceptions, a trustee in bankruptcy may avoid any transfers of an interest in the debtor’s property that is made on or within 90 days before filing the bankruptcy petition. ... read more

by Lauren T. Konagel | Dec 22, 2022 | Business and Personal, Lauren T. Konagel

In Indiana, all businesses and organizations, including churches and nonprofit organizations, are required to file business tangible personal property returns every year with the assessor’s office of the applicable county. Business personal property consists of all... read more

by Burke Costanza & Carberry LLP | Apr 12, 2022 | Business & Commercial Litigation, Business and Personal, Estate Planning, Litigation, News

Northwest Indiana Business Magazine Has Announced Best of Business Awards 2022. Each year, the magazine surveys their readers asking them to vote for the best businesses throughout Northwest Indiana and Greater South Bend / Mishawaka. The survey provides readers... read more

by Schuyler D. Geller | Jul 30, 2021 | Arbitration, Business and Personal, Litigation, News

BCC congratulates Attorney Schuyler D. Geller, who has recently been appointed to FINRA’s Roster of Arbitrators. FINRA is the governing body that resolves disputes in the financial services industry. Attorney Geller has been representing both customers and... read more

by Burke Costanza & Carberry LLP | Mar 9, 2021 | Business & Commercial Litigation, Business and Personal, Litigation, News

Northwest Indiana Business Magazine Has Announced Best of Business Awards 2021. Each year, the magazine surveys their readers asking them to vote for the best businesses throughout Northwest Indiana and Greater South Bend / Mishawaka. The survey provides readers... read more

by Chad W. Nally | Nov 24, 2020 | Business and Personal

Whether you have already had your Paycheck Protection Program (PPP) loan forgiven, or you are waiting for news from your lender, it is important to start planning ahead for the tax consequences of PPP forgiveness. Fortunately, there is something you can do to ensure... read more